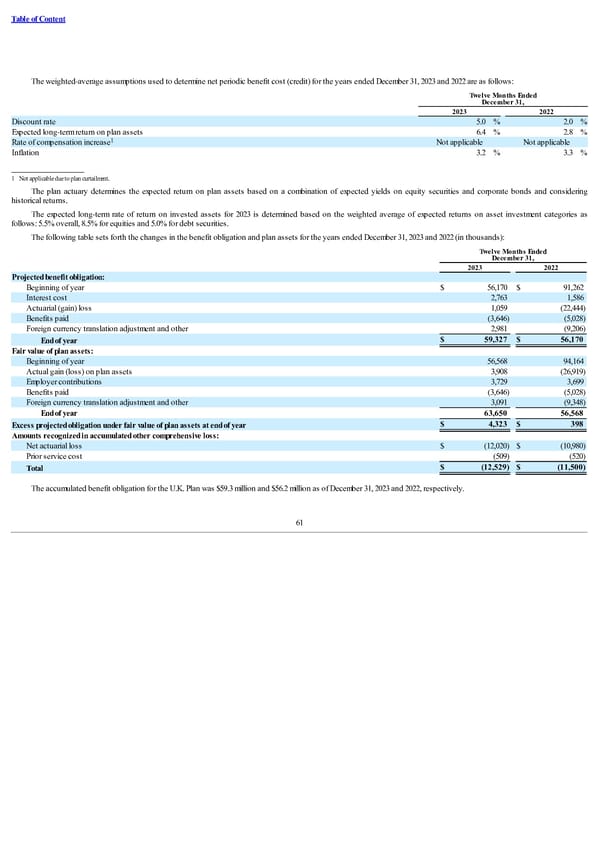

Table of Content The weighted-average assumptions used to determine net periodic benefit cost (credit) for the years ended December 31, 2023 and 2022 are as follows: Twelve Months Ended December 31, 2023 2022 Discount rate 5.0 % 2.0 % Expected long-term return on plan assets 6.4 % 2.8 % 1 Rate of compensation increase Not applicable Not applicable Inflation 3.2 % 3.3 % _______________ 1 Not applicable due to plan curtailment. The plan actuary determines the expected return on plan assets based on a combination of expected yields on equity securities and corporate bonds and considering historical returns. The expected long-term rate of return on invested assets for 2023 is determined based on the weighted average of expected returns on asset investment categories as follows: 5.5% overall, 8.5% for equities and 5.0% for debt securities. The following table sets forth the changes in the benefit obligation and plan assets for the years ended December 31, 2023 and 2022 (in thousands): Twelve Months Ended December 31, 2023 2022 Projected benefit obligation: Beginning of year $ 56,170 $ 91,262 Interest cost 2,763 1,586 Actuarial (gain) loss 1,059 (22,444) Benefits paid (3,646) (5,028) Foreign currency translation adjustment and other 2,981 (9,206) $ 59,327 $ 56,170 End of year Fair value of plan assets: Beginning of year 56,568 94,164 Actual gain (loss) on plan assets 3,908 (26,919) Employer contributions 3,729 3,699 Benefits paid (3,646) (5,028) Foreign currency translation adjustment and other 3,091 (9,348) End of year 63,650 56,568 $ 4,323 $ 398 Excess projected obligation under fair value of plan assets at end of year Amounts recognized in accumulated other comprehensive loss: Net actuarial loss $ (12,020) $ (10,980) Prior service cost (509) (520) $ (12,529) $ (11,500) Total The accumulated benefit obligation for the U.K. Plan was $59.3 million and $56.2 million as of December 31, 2023 and 2022, respectively. 61

Form 10-K Page 65 Page 67

Form 10-K Page 65 Page 67